Merchant onboarding in Europe is often perceived as slow or inconsistent, especially by businesses eager to start processing payments. In reality, onboarding is not a simple administrative step but a structured risk validation process shaped by regulation, banking requirements, and internal PSP controls. Each document request and review stage exists to answer a fundamental question: can this merchant be supported safely and compliantly? Understanding what drives onboarding timelines helps merchants prepare properly and avoid unnecessary delays.

- How Merchant Onboarding Works in Europe (High-Level)

- Core Documentation Required for European Merchant Onboarding

- Transaction and Business Model Documentation

- Risk Checks That Influence Onboarding Timelines

- Why Onboarding Timelines Vary Between PSPs and Countries

- Common Causes of Delays in European Merchant Onboarding

- What Merchants Should Understand About European Onboarding Timelines

- Conclusion

- FAQs

How Merchant Onboarding Works in Europe (High-Level)

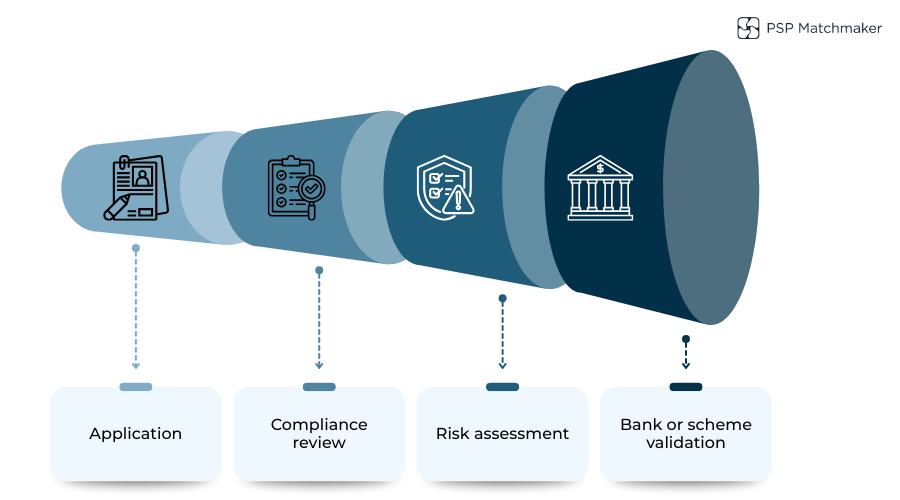

European merchant onboarding typically follows a sequential process rather than a parallel one. Most PSPs and acquiring partners move through the same core stages:

Initial application submission

KYB and compliance review

Risk and business model assessment

Bank or scheme validation, where required

Each stage depends on the outcome of the previous one. This is why onboarding rarely progresses “all at once”. Importantly, there is a difference between an application being submitted and a merchant being risk-cleared. Submission only confirms receipt of information; clearance means the PSP and its banking partners are satisfied with both documentation and risk exposure. Delays usually occur when clarification is required before moving to the next stage.

Core Documentation Required for European Merchant Onboarding

Business and Legal Documentation

The first step in onboarding is establishing the merchant’s legal identity. PSPs need to confirm that the business exists, is properly registered, and operates in permitted jurisdictions. Commonly required documents include a certificate of incorporation, company registry extracts, and confirmation of registered and operating addresses.

These documents form the foundation of KYB checks. If they are outdated, inconsistent, or incomplete, onboarding typically pauses until they are corrected. Even minor discrepancies, such as address mismatches, can trigger follow-up reviews.

Ownership and Control Information

European AML rules require transparency around who ultimately controls a business. Merchants are therefore asked to provide UBO declarations, shareholding structures, and identification for directors and beneficial owners.

Complex ownership chains, particularly those involving multiple jurisdictions or holding companies, often extend review timelines due to additional verification steps.

Transaction and Business Model Documentation

Beyond legal identity, PSPs need to understand how the business actually operates. This includes a clear description of products and services, as well as an explanation of the customer journey from payment initiation to fulfilment.

Fund flow documentation is particularly important. Merchants are often asked to explain:

How payments are received (pay-ins)

Whether funds are held or pooled at any stage

How and when payouts or settlements occur

This matters because PSPs assess where financial risk and liability sit at each point in the flow. Ambiguous or poorly explained flows almost always trigger clarification cycles, which extend onboarding timelines even when the underlying business is acceptable.

Risk Checks That Influence Onboarding Timelines

AML and Sanctions Screening

All European PSPs must conduct AML and sanctions screening on the merchant entity, as well as on directors and UBOs. Screening covers sanctions lists, politically exposed person databases, and adverse media sources. Any potential match, even a false positive, usually requires manual review and slows the process.

Business Model Risk Assessment

PSPs also assess the inherent risk of the business model itself. Factors such as expected chargeback exposure, refund dependency, and customer geography all influence risk classification. Merchants operating in regulated or higher-risk sectors typically face deeper scrutiny and longer approval chains.

Ongoing Monitoring Readiness

Onboarding is not only about initial approval. PSPs evaluate whether transactions can be effectively monitored post-approval. If a model makes monitoring difficult, additional controls or documentation may be required before approval is granted.

Why Onboarding Timelines Vary Between PSPs and Countries

Onboarding timelines vary because PSPs do not all operate under identical constraints. Differences in risk appetite, sponsor bank involvement, and internal approval thresholds all affect speed.

In some countries, local regulators expect more detailed validation, while in others, sponsor banks retain final approval authority.

As a result, the same merchant can experience very different timelines depending on the provider they apply to. This does not necessarily reflect quality or efficiency; it reflects how closely a merchant’s profile aligns with a PSP’s risk framework and banking setup.

Common Causes of Delays in European Merchant Onboarding

Most onboarding delays are avoidable. The most common causes include missing or outdated documents, inconsistent information across submissions, and unclear explanations of how the business operates. Delays also arise when merchants respond slowly to clarification requests or provide partial answers that trigger further questions.

In many cases, onboarding stalls not because the merchant is unsuitable, but because risk teams cannot confidently complete their assessment with the information provided. Each clarification cycle adds time.

What Merchants Should Understand About European Onboarding Timelines

Merchant onboarding in Europe is fundamentally a risk validation exercise, not a box-ticking formality. The quality and clarity of documentation directly influence how quickly risk teams can reach a decision. Delays usually indicate a need for clarification rather than an impending rejection.

Merchants that prepare documentation upfront, explain their business model clearly, and align with providers whose risk appetite matches their profile typically experience smoother onboarding. Preparation reduces back-and-forth and shortens approval cycles.

Conclusion

European merchant onboarding timelines are shaped by documentation quality, risk assessment depth, and provider-specific controls. While the process can feel slow, it is designed to ensure sustainable, compliant payment relationships. Merchants who understand what PSPs are validating and why are far better positioned to navigate onboarding efficiently and avoid unnecessary delays.

FAQs

1. Why does merchant onboarding in Europe take longer than expected?

Merchant onboarding in Europe is a regulated risk validation process, not a simple account setup. PSPs must verify legal identity, ownership, business model risk, and compliance obligations before approval, which naturally takes time.

2. What documentation is always required during European merchant onboarding?

Most PSPs require core business documents such as incorporation records, company registry extracts, registered address details, and ownership information for directors and UBOs. Additional documents depend on the merchant’s risk profile and sector.

3. Do all PSPs require the same onboarding documents?

No. While there is a common baseline, documentation requirements vary by PSP, sponsor bank, and country. Some providers request deeper operational or financial detail depending on internal risk appetite.

4. What causes the biggest delays during onboarding?

The most common causes are missing or outdated documents, inconsistent information across submissions, and unclear explanations of how payments and fund flows work. Slow responses to clarification requests also extend timelines.

5. What is the difference between application submission and approval?

Submitting an application only confirms that documents have been received. Approval occurs after compliance, risk, and (where applicable) bank-level reviews are completed and the merchant is formally risk-cleared.

6. How do risk checks affect onboarding timelines?

Risk checks such as AML screening, sanctions checks, and business model assessments often require manual review. Any potential match or uncertainty typically triggers additional verification, which extends timelines.

7. Why can the same merchant be approved quickly by one PSP but slowly by another?

PSPs differ in risk appetite, internal workflows, and banking partners. As a result, the same merchant profile can align well with one provider’s framework and poorly with another’s, leading to very different timelines.

8. Does being a high-risk or regulated merchant always mean delays?

Not always, but higher-risk or regulated businesses usually face more detailed review. This often includes additional documentation, internal escalation, or sponsor bank approval, which increases onboarding time.

9. Can merchants speed up the onboarding process?

Yes, Clear documentation, consistent information, detailed business model explanations, and prompt responses to clarification requests significantly reduce iteration cycles and improve approval speed.

10. Does a long onboarding process mean rejection is likely?

No. In most cases, delays reflect clarification or validation needs rather than an intent to decline. Many merchants are approved after additional information is reviewed and risk questions are resolved.

Leave a Reply