Pay by Bank works well in the UK. That statement is true and also incomplete. What matters more is where it works cleanly and where it quietly changes the shape of a payment in ways merchants don’t always anticipate. Too often, Pay by Bank is discussed as a cheaper card alternative or a regulatory success story. Neither framing is particularly useful once it reaches a real checkout.

The practical question for merchants isn’t whether Pay by Bank is viable. It’s whether the payment flow they’re offering actually benefits from the way Pay by Bank behaves.

What Pay by Bank Means in the UK

In the UK, Pay by Bank isn’t a branded product and it isn’t a scheme. It’s an outcome of Open Banking being operational enough to support payment initiation at scale.

That distinction matters. A Pay by Bank transaction doesn’t ask a customer for permission to pull funds later. It asks them to actively approve a transfer, inside their own bank, at that moment. The bank confirms identity. The bank authorises the movement of money. Everyone else steps aside.

There are no card rails in the background. No network rules waiting downstream. No dispute framework that assumes ambiguity around customer intent.

This is why Pay by Bank often feels decisive.

Once approved, the payment is done.

Once declined or abandoned, there is very little to negotiate.

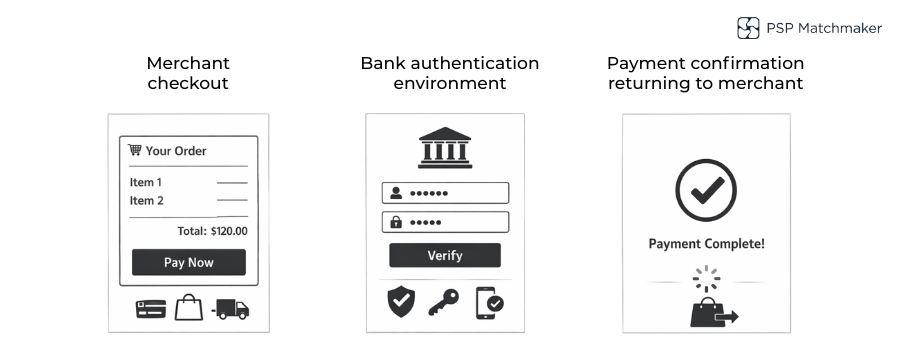

How Pay by Bank Transactions Work

A Pay by Bank payment doesn’t progress in a straight line. It jumps contexts.

The merchant starts the process, but does not control the middle of it. The customer leaves the checkout, enters their bank’s environment, and completes the action there or doesn’t. What the merchant sees next is a result, not a journey.

What typically exists between selection and completion is not one moment, but several states:

- A redirect into the bank

- An authentication decision owned by the bank

- An explicit approval or exit by the customer

- A confirmation signal returned through the PSP

Settlement sits elsewhere, often later, sometimes quietly.

This separation is the source of most operational misunderstandings. Pay by Bank confirms quickly. It does not always resolve quickly. And merchants only tend to notice the difference when expectations are built on card logic instead.

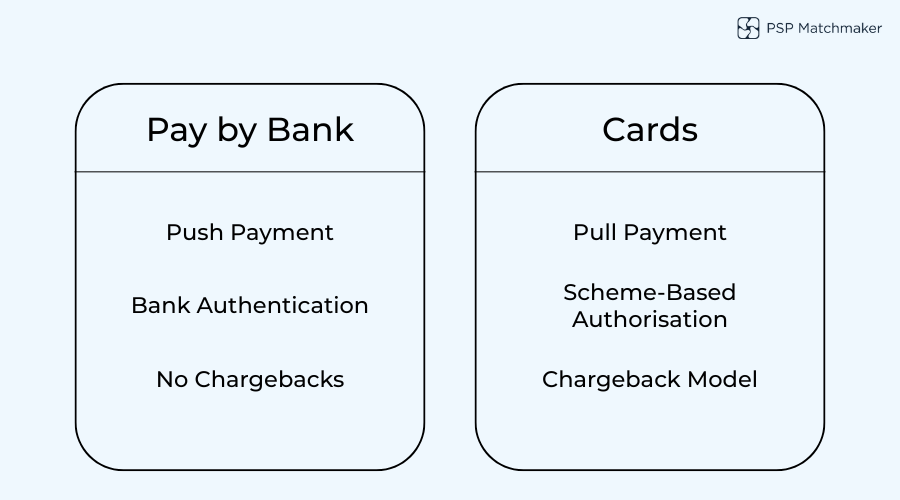

How Pay by Bank Differs from Card Payments

The difference between Pay by Bank and cards isn’t mainly about cost or speed. It’s about who is doing the authorising and what happens when something goes wrong.

Card payments operate on assumption. The system assumes permission until it is challenged later, often through a dispute or chargeback. Pay by Bank does the opposite. It requires the customer to be present, authenticated, and explicit at the moment the money moves.

That creates a different operating reality.

There is no pull request.

No delayed reversal mechanism.

No scheme-layer arbitration waiting in the background.

Refunds still happen, but they are deliberate actions, not automated outcomes of a dispute flow. This is why Pay by Bank often feels cleaner operationally and harsher when expectations are shaped by card behaviour.

Common Merchant Use Cases for Pay by Bank

Pay by Bank tends to work best when the payment is intentional and contained. Not recurring. Not speculative. Not loosely authorised.

Merchants use it effectively when:

- The customer already trusts the brand

- The payment unlocks something immediately

- The transaction does not need post-authorisation flexibility

- Disputes are operationally expensive or undesirable

Account funding, top-ups, and one-off purchases fit this profile well. The customer knows what they are doing, the bank confirms it, and the payment concludes without ambiguity.

Where Pay by Bank struggles is not in execution, but in expectation. When it’s used in flows that quietly rely on card-era assumptions, friction shows up later.

Situations Where Cards May Be More Suitable

Cards still outperform Pay by Bank in situations where optionality matters more than certainty.

Subscriptions are an obvious example. So are delayed fulfilment models, where goods or services are delivered long after payment. In these cases, the card ecosystem’s tolerance for adjustment, reversal, and dispute becomes a feature, not a flaw.

Cards also remain dominant when:

Customers expect stored credentials

Speed of repeat payment matters more than explicit consent

Refunds are frequent, partial, or negotiable

- Refunds are frequent, partial, or negotiable

Pay by Bank does not fail in these scenarios it simply does not bend.

Operational Considerations for Merchants

From an operational standpoint, Pay by Bank introduces fewer moving parts, but less flexibility.

Confirmation arrives quickly. Settlement may not. Reconciliation depends on bank references rather than familiar card identifiers. Support teams must handle payment issues without leaning on chargeback logic.

The biggest variable is the PSP layer. Not all Open Banking implementations are equal, and differences show up in:

- Status reliability

- Settlement handling

- Reporting clarity

- How cleanly failures are communicated

Merchants who underestimate this layer often blame the payment method for what is actually an implementation issue.

Adoption and Customer Behaviour in the UK

UK consumers are broadly comfortable with bank-based authentication. That comfort is what makes Pay by Bank viable at scale.

Still, experience is uneven. Some banks deliver clean, fast approval flows. Others introduce friction through redirects, device switching, or unclear prompts. Customers don’t blame the bank. They blame the checkout.

Adoption therefore isn’t just about awareness. It’s about how confidently the payment is framed, and how well the experience survives the handoff from merchant to bank and back again.

What Merchants Should Understand When Comparing Pay by Bank and Cards

Pay by Bank and cards are not competitors in the traditional sense. They answer different operational questions.

Cards optimise for convenience and continuity.

Pay by Bank optimises for certainty and intent.

Outcomes depend on:

- Customer behaviour at the moment of payment

- Bank experience quality

- PSP execution

- How closely the payment flow matches the method’s strengths

Many UK merchants support both, not because one is better, but because neither is sufficient on its own.

Conclusion

Pay by Bank has reached a point in the UK where it no longer needs justification. The infrastructure exists, customer familiarity is real, and the payment flow works as intended. What remains inconsistent is not capability, but judgment.

For merchants, the real challenge is recognising that Pay by Bank does not behave like cards and does not need to. It introduces clarity at the moment of payment, but it also removes some of the flexibility that card-based models have normalised over time. That trade-off is neither good nor bad by default; it simply needs to be understood.

Merchants that see Pay by Bank as a precision tool, rather than a universal replacement, tend to extract the most value from it. Those that design payment flow around its strengths: explicit consent, bank-level authentication, and reduced ambiguity avoid the operational surprises that come from applying card logic where it no longer fits.In practice, the most resilient UK payment setups are not built around choosing sides. They are built around choosing when certainty matters more than convenience, and when it does not.

FAQs

1. Is Pay by Bank the same as Open Banking payments in the UK?

Pay by Bank in the UK is typically powered by Open Banking payment initiation, but the term describes how the payment is experienced rather than the regulation behind it. Customers approve a bank transfer directly inside their bank, which is what defines the behaviour merchants see.

2. Are Pay by Bank payments instant once approved?

Approval is usually fast, but that does not always mean funds are immediately settled. Confirmation and settlement are separate steps, and timing depends on bank connectivity and the PSP’s settlement model.

3. Can Pay by Bank payments be charged back like card payments?

No. Pay by Bank does not operate within a card scheme, so there is no chargeback framework. Refunds are handled as new bank transfers initiated by the merchant.

4. Why do some Pay by Bank payments feel less predictable than cards?

Because the middle of the payment flow happens inside the customer’s bank. Merchants do not control authentication, UX, or completion behaviour in the same way they do with card checkouts.

5. Is Pay by Bank cheaper than cards for merchants?

Often, but not universally. Cost depends on the PSP, transaction volume, and settlement setup. The bigger operational difference is not price, but how disputes and failures are handled.

6. Does Pay by Bank work well for repeat or subscription payments?

In most cases, no. Pay by Bank is best suited to one-off, intentional payments. Consistent recurring payment support is still uneven across banks.

7. Why do merchants still need cards if Pay by Bank is available?

Cards provide flexibility that Pay by Bank does not, particularly for delayed fulfilment, customer-initiated disputes, and stored credentials. Many merchants need both to cover different behaviours.

8. How important is the PSP when offering Pay by Bank?

Critical. PSPs determine how reliably payment status is returned, how settlement is handled, and how clearly issues are reported. Differences between providers are often mistaken for payment method issues.

9. Do customers trust Pay by Bank in the UK?

Generally, yes. Trust is driven by bank-level authentication. However, trust does not guarantee completion; poor handoffs or unclear messaging can still cause drop-off.

10. Should Pay by Bank replace cards at checkout?

Not as a default. Pay by Bank works best when used intentionally, for specific flows where certainty and explicit consent matter more than flexibility or speed of repeat payment.

Leave a Reply