Australia’s shift to real-time payments is often discussed through two closely linked terms: NPP and PayID. While they are frequently mentioned together, they serve very different roles within the payments ecosystem. One represents national payment infrastructure, while the other functions as a usability layer designed to simplify how bank transfers are initiated. This overlap has created confusion, particularly around how real-time payments are actually enabled. This blog explains how Australia’s real-time bank transfers work in practice, clarifying the relationship between NPP and PayID and outlining how funds move between accounts in real time.

Australia’s Real-Time Payments Framework

Australia built a real-time payments framework to modernise domestic bank transfers and move beyond the limitations of batch-based clearing systems. The objective was not to create a consumer-facing product, but to establish shared infrastructure that all participating banks could rely on.

At the centre of this framework is the New Payments Platform (NPP). NPP functions as foundational infrastructure rather than a payment method that consumers actively “choose”. It enables participating financial institutions to exchange payment messages and settle funds in real time, forming the backbone for multiple payment services.

Key elements of Australia’s real-time payments framework include:

Industry-owned infrastructure

National real-time payment rail

24/7 availability, including weekends

Direct bank-to-bank settlement

Oversight by the Reserve Bank of Australia

This infrastructure-first approach allows innovation to occur at the service layer while keeping core settlement stable and consistent.

PayID and Its Role Within the NPP

While NPP provides the underlying rails, PayID addresses a different problem: usability. Traditional bank transfers require customers to enter BSB and account numbers, which creates friction and increases error risk. PayID sits on top of the NPP to simplify how recipients are identified.

PayID is a unique identifier that is securely linked to a bank account.

Instead of sharing account details, users can send or receive payments using a recognisable identifier that resolves to the correct account before the payment is sent.

PayID improves the payment experience by:

- Removing the need to enter BSB and account numbers

- Reducing misdirected payments through pre-payment validation

- Allowing users to verify the recipient name before confirming

Common PayID identifier types include:

- Mobile number

- Email address

- Business identifier

Once a PayID is resolved, the payment is routed through the NPP using the linked account details.

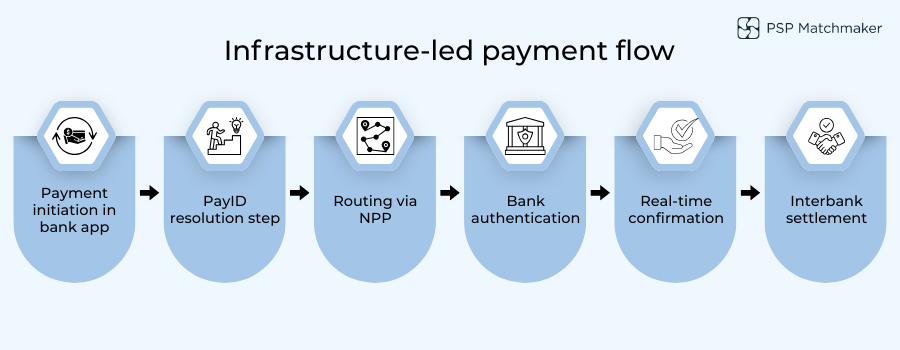

How Real-Time Bank Transfers Are Processed

Real-time transfers using NPP and PayID follow a defined sequence. Steps are used here because the process is linear and benefits from clear separation.

Payment initiation

The customer starts a transfer within their bank’s app, entering a PayID or selecting a saved recipient.

PayID resolution

The system confirms which bank account the PayID is linked to and displays recipient details.

Routing via NPP

Payment instructions are sent through the NPP infrastructure to the receiving institution.

Customer authentication

The payer authorises the transaction using their bank’s security controls.

Real-time confirmation

Both parties receive near-instant confirmation that the payment has succeeded.

Interbank settlement

Funds are settled between institutions through NPP-supported settlement arrangements.

This flow enables speed while keeping banks responsible for authentication and approval.

How NPP and PayID Are Used in Practice

Consumer Payment Scenarios

Consumers primarily use PayID-enabled transfers for everyday account-to-account payments. Common scenarios include peer-to-peer transfers between friends or family, bill and service payments, and ad hoc transfers where immediacy matters. The ability to confirm recipient details before sending funds has helped build confidence in real-time transfers.

Business and Merchant Scenarios

Businesses use NPP and PayID for customer payments, refunds, and payouts where real-time confirmation improves cash flow visibility. PayID is also used for account funding and internal transfers. Faster confirmation supports quicker reconciliation, particularly for businesses handling high transaction volumes or time-sensitive services.

The same infrastructure supports both audiences, but usage patterns differ based on operational needs.

Operational Characteristics and Practical Limitations

Although payments are processed in real time, this does not mean they are unlimited or reversible. NPP and PayID introduce operational characteristics that differ from card-based payments.

Key practical considerations include:

- Push-payment structure, initiated by the payer

- No card-style chargeback mechanism

- Refunds processed as new outbound transfers

- Transaction limits set by individual banks

- Participation and feature differences across institutions

- Reference-based reconciliation rather than batch files

Because banks control limits and authentication, capabilities can vary between institutions. Businesses must also manage refunds proactively, as there is no automatic reversal process. Understanding these constraints is essential to avoid treating real-time transfers as a direct replacement for all payment methods.

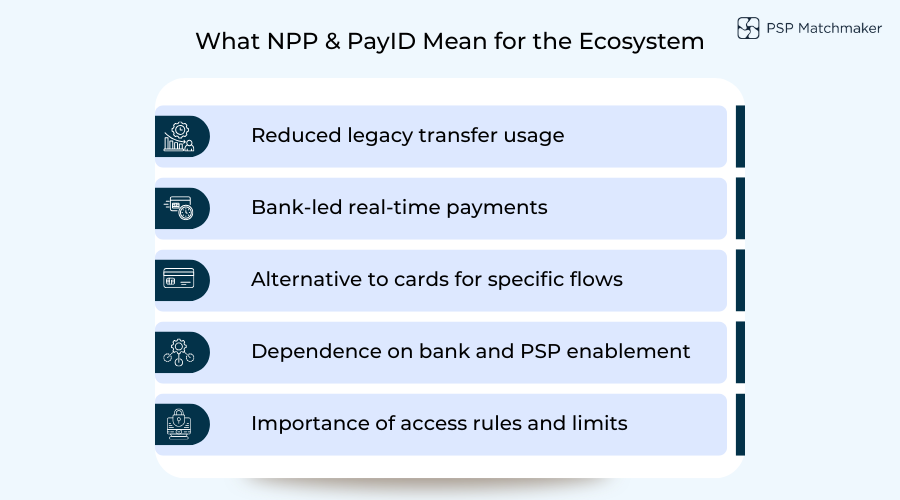

What NPP and PayID Mean for Australia’s Payments Ecosystem

NPP and PayID represent a broader shift towards infrastructure-led innovation in Australia’s domestic payments landscape. Instead of building isolated products, the ecosystem has focused on shared rails that multiple services can leverage.

Key takeaways for the payments ecosystem include:

- Reduced reliance on legacy batch transfers

- A viable alternative to cards for certain payment flows

- Greater emphasis on bank and PSP enablement

- The need to understand access rules and limits

While adoption is widespread, capabilities are not uniform across all banks. As a result, businesses benefit most when they align payment strategy with how the infrastructure actually operates rather than how it is marketed.

Conclusion

NPP and PayID combine infrastructure and identity to enable seamless, real-time bank transfers across Australia. Together, they form a central pillar of the modern payments landscape, offering merchants a secure, irrevocable way to accept funds.However, navigating the access rules and finding a provider that supports these features especially for high-risk or international businesses can be complex. At PSP Matchmaker, we specialize in connecting businesses with the right payment partners to unlock the full potential of regional infrastructure like the NPP.

FAQs

1. Are NPP and PayID the same thing?

No. NPP and PayID serve different roles. NPP is the underlying real-time payments infrastructure that enables funds to move between banks. PayID is an identification service built on top of NPP that makes it easier to initiate payments by replacing BSB and account numbers with simple identifiers.

2. Does using PayID automatically mean payments are real time?

In most cases, yes, but the real-time capability comes from NPP rather than PayID itself. PayID simplifies recipient identification, while NPP enables the actual real-time transfer and settlement between banks.

3. Can NPP be used without PayID?

Yes. Banks can process real-time payments over NPP using traditional account details. PayID is optional and exists to improve usability, not to enable real-time processing on its own.

4. Why do some PayID payments fail or get delayed?

Failures or delays are usually caused by bank-specific controls rather than the NPP infrastructure itself. Transaction limits, compliance checks, customer authentication issues, or temporary bank outages can all affect outcomes.

5. Are NPP payments reversible if sent in error?

No. NPP payments are push payments and do not include a reversal or chargeback mechanism. If funds are sent to the wrong recipient, recovery depends on the receiving bank and the recipient’s cooperation.

6. How do businesses typically use PayID?

Businesses commonly use PayID for customer payments, refunds, account funding, and internal transfers. Using a business identifier allows customers to pay without requesting bank account details, which can improve trust and reduce errors.

7. Is PayID suitable as a replacement for card payments?

PayID can replace cards in certain scenarios, such as account-to-account transfers or low-dispute payment flows. However, it does not support card-style protections like chargebacks, so it is not suitable for all transaction types.

8. Do all Australian banks support the same PayID features?

No. While most major banks support PayID, features such as transaction limits, identifier types, and customer experience can vary. Businesses should not assume uniform capability across all institutions.

9. How are refunds handled for NPP and PayID payments?

Refunds are typically processed as new outbound transfers rather than reversals of the original payment. This requires businesses to maintain accurate records and have clear refund processes in place.

10. Does NPP support high-value transactions?

NPP can support higher-value payments, but limits are set by individual banks and may differ between consumer and business accounts. Businesses should confirm applicable limits with their banking or PSP partners.

11. Is PayID mandatory for businesses operating in Australia?

No. PayID is not mandatory, but it is widely used and increasingly expected in certain payment scenarios. Whether it is appropriate depends on the business model, payment flows, and risk tolerance.

12. Why is understanding the difference between NPP and PayID important for merchants?

Confusing infrastructure with identifiers can lead to incorrect assumptions about speed, reversibility, and availability. Understanding how NPP and PayID work together helps merchants design realistic payment flows and avoid operational issues.

Leave a Reply