Open Banking payments often branded as “Pay by Bank” are increasingly discussed as a way for merchants to reduce card costs, improve authorisation outcomes, and give customers a more direct way to pay from their bank account. In parts of Europe, they are already a meaningful payment rail for specific use cases. In others, they remain an emerging option with uneven customer awareness and inconsistent bank experience.

The important point for merchants is that adoption is not moving at the same speed everywhere, and it is not driven by regulation alone. It is driven by what customers see at checkout, how smoothly banks handle authentication, and whether PSPs can deliver a stable, predictable payment experience.

- What Are Open Banking Payments in the European Context?

- How Open Banking Payments Are Used by Merchants Today

- Common Merchant Use Cases

- Use Cases That Are Still Limited

- Adoption of Open Banking Payments Across Europe

- The Role of Banks and PSPs in Adoption

- What Merchants Should Understand About Open Banking Adoption

- Conclusion

- FAQs

What Are Open Banking Payments in the European Context?

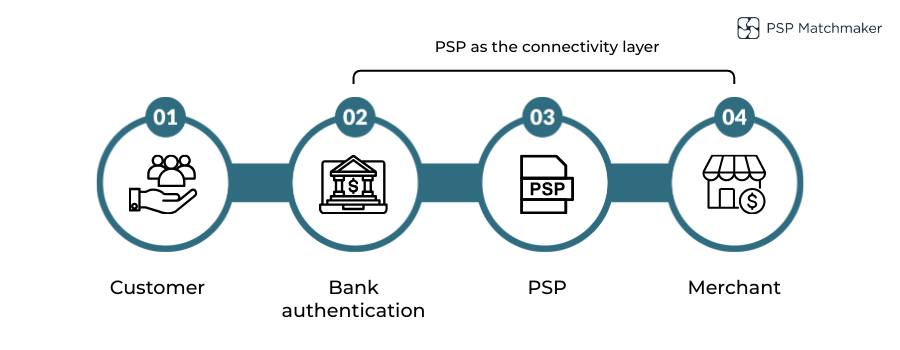

In simple terms, Open Banking payments are account-to-account (A2A) payments initiated via bank APIs. Instead of the customer typing in bank details or using a card, they select a Pay-by-Bank option, authenticate with their bank, and approve a transfer.

Across the EU, Open Banking was materially enabled by PSD2, which created the regulatory basis for licensed third parties to access payment accounts (with customer consent) and initiate payments.

In the merchant context, Open Banking payments are most commonly associated with payment initiation: the customer approves a push payment from their bank account to the merchant.

How Open Banking Payments Differ from Cards

Open Banking payments are structurally different from card payments, and that difference explains both the advantages and the trade-offs.

- Cards are “pull” payments: the merchant (via acquirer) requests money through card networks.

Because the card schemes are not involved, Open Banking payments typically avoid scheme rules and interchange mechanics. That can change the cost profile and risk profile but it also means merchants should not assume they will get “card-like” protections and workflows.

How Open Banking Payments Are Used by Merchants Today

Merchants using Open Banking payments in Europe are generally doing so for situations where the A2A model creates a clear operational or commercial benefit.

You most often see Open Banking payments used for:

Account funding and wallet top-ups

This is one of the most natural fits because confirmation can be near-real-time and the payment is authorised directly in the customer’s bank environment. It reduces reliance on cards for “cash-like” use cases where card acceptance can be fragile.

High-frequency, cost-sensitive transactions

Where card fees are a meaningful margin item for example in certain digital services Pay-by-Bank can be positioned as a cheaper alternative, especially if the PSP can deliver a smooth experience.

First-time payments that lead into longer-term relationships

Some merchants use Pay-by-Bank for initial deposits, invoices, or higher-trust moments, then keep cards and wallets available for convenience-driven repeat spend. (In a few markets, newer models like variable recurring payments are developing, but they are not consistently available across Europe yet.)

Situations where lower chargeback exposure is a feature:

Because Open Banking is typically a push payment, it does not operate with the same chargeback model as cards. That can reduce one kind of downstream operational risk but it also changes how refunds and disputes need to be handled.

Common Merchant Use Cases

Open Banking payments are most effective where the account-to-account model aligns naturally with how money is exchanged and how risk is managed. In Europe today, merchants tend to adopt Pay-by-Bank in use cases where immediacy, cost control, or reduced dispute exposure clearly outweigh the convenience of cards.

Common scenarios include:

- Account funding and balance top-ups: This remains one of the strongest use cases. Customers can move funds directly into an account or wallet with near-real-time confirmation, allowing merchants to credit balances quickly without relying on cards for cash-like activity.

- Invoice and bill payments: Open Banking works well for invoice-based flows, where the customer expects to pay from their bank account and values clear payment references. The structured nature of these payments also supports cleaner reconciliation for merchants.

- Low-dispute payment scenarios: Where transactions are straightforward and unlikely to be contested, Open Banking reduces exposure to chargeback-driven processes. This makes it attractive in environments where disputes are rare and customer intent is clear.

Use Cases That Are Still Limited

While adoption is growing, Open Banking payments are not yet suitable for every payment scenario. Certain models remain constrained by regulatory, technical, or user-experience limitations.

Areas where usage is still limited include:

Recurring subscriptions

Most Open Banking payment flows are designed for one-off authorisations. Although developments such as variable recurring payments exist in parts of Europe, they are not yet consistently available or widely supported across banks.

Delayed fulfilment models

Where goods or services are delivered significantly later, merchants often rely on card mechanisms that allow for post-authorisation adjustments, refunds, or disputes. Open Banking’s push-payment structure makes these models harder to support cleanly.

Complex, refund-heavy flows

Because refunds must be processed as new bank transfers, Open Banking can introduce operational overhead in environments with frequent partial refunds, reversals, or customer-initiated changes.

For most European merchants today, these limitations mean Open Banking works best when used selectively, alongside cards and other payment methods, rather than as a universal solution.

Adoption of Open Banking Payments Across Europe

Adoption across Europe is best described as growing, but uneven.

- The UK is often referenced as a leading market in Open Banking usage, with published ecosystem metrics showing continued growth in users and payment activity.

- Across the EU, Open Banking adoption varies heavily by local banking execution, consumer habits, and how widely Pay-by-Bank is presented at checkout (and how well it works when customers try it).

A practical merchant takeaway is that “Europe” is not one Open Banking market. If your customer base is concentrated in one or two countries, adoption may be strong enough to justify a prominent checkout placement.

If you sell across many countries, you may need to treat Pay-by-Bank as an opportunistic method with routing and fallbacks.

Consumer Awareness and Behaviour

Consumer awareness is improving, but it is still not universal. Where Pay-by-Bank is well presented and reliably delivered, customers learn to trust it because:

- The customer authenticates directly with their own bank

- The flow feels familiar (bank login / strong customer authentication)

- The payment is clearly tied to the customer’s bank account

That said, user experience can vary by bank and provider. Even when the merchant’s side is polished, the in-bank screens, redirects, and approval steps can feel different depending on the customer’s bank which is one reason adoption grows faster in markets with more consistent bank UX.

The Role of Banks and PSPs in Adoption

PSD2 created the foundation, but it did not create perfectly uniform APIs. In practice:

- Not all banks expose identical payment initiation capabilities

- Uptime and reliability can vary

- The “last mile” of UX sits with the customer’s bank

Industry discussions and reports have repeatedly highlighted that API performance and consistency are a real determinant of merchant experience (even when the scheme concept is strong).

Payment Confirmation and Settlement

Many Open Banking flows can deliver real-time or near-real-time payment confirmation which is why they work well for account funding and time-sensitive access.

Settlement, however, may still depend on:

- Bank processing mechanics

- The PSP’s settlement model

- The merchant’s own treasury setup

So “confirmed” and “available to use” are not always the same moment a distinction merchants should build into their operational expectations.

Refund Handling

Open Banking payments typically do not behave like cards when something goes wrong. There is usually no card-style chargeback mechanism. Refunds are normally processed as a new bank transfer back to the customer.

That changes customer support and dispute handling. Merchants should be prepared to explain the process clearly and maintain robust internal workflows for refund approvals and audit trails.

Reconciliation and Reporting

Reconciliation is usually driven by bank references and PSP reporting. While that can be clean when implemented well, formats and detail levels vary by provider, so finance teams should review:

- Whether unique payment references are consistent end-to-end

- How pending/confirmed/failed states are reported

- How refunds are represented in reports

What Merchants Should Understand About Open Banking Adoption

Open Banking payments are clearly growing, but they are not a universal replacement for cards.

They tend to perform best when:

- The customer’s bank experience is smooth and familiar

- The PSP has strong connectivity and stable confirmation handling

- The merchant uses Pay-by-Bank for scenarios that match the A2A model (funding, invoices, cost-sensitive flows)

In most European merchant setups today, Open Banking works best as a complement to cards and wallets not a full substitute because adoption and experience still vary meaningfully by country and bank.

Conclusion

Open Banking payments in Europe have moved well beyond theory. They are actively used by merchants today, particularly where instant confirmation, cost control, or reduced chargeback exposure matter. But adoption remains uneven, and the real determinant of success is not the regulation it is execution: bank UX, API reliability, and PSP capability.

For merchants, the practical approach is to treat Pay-by-Bank as a strategic addition: deploy it where it improves outcomes, measure performance by market, and build the right fallback routes so customers never hit a dead end at checkout.

FAQs

1. What are Open Banking payments in simple terms?

Open Banking payments allow customers to pay directly from their bank account using a Pay-by-Bank option. The customer authorises the payment within their own banking environment, and funds are transferred account to account without using card networks.

2. Are Open Banking payments the same as instant bank transfers?

Not exactly. Open Banking payments initiate a bank transfer through APIs, while instant transfers depend on the underlying payment scheme. Some Open Banking payments are confirmed in near real time, but settlement speed can vary by bank and PSP.

3. How widespread is Open Banking payment adoption in Europe?

Adoption is growing but uneven. Some markets show strong usage and consumer familiarity, while others still have limited uptake due to inconsistent bank experience or lower awareness. Europe should be viewed as multiple Open Banking markets rather than a single one.

4. Why do Open Banking payments work better in some countries than others?

Differences in bank API quality, uptime, user experience, and local promotion all affect adoption. Markets where banks deliver smoother authentication flows tend to see higher consumer trust and repeat usage.

5. Are Open Banking payments cheaper than card payments for merchants?

In many cases, yes. Open Banking payments typically avoid card scheme fees and interchange. However, pricing depends on the PSP, transaction volumes, and the specific markets involved.

6. Can Open Banking payments be charged back like card payments?

No. Open Banking payments usually do not support card-style chargebacks. Payments are customer-authorised push transfers, so refunds must be handled manually by the merchant as new bank transfers.

7. What happens if a customer abandons the payment during bank authentication?

If the customer does not complete authentication, the payment is not executed. Depending on the PSP setup, the merchant may receive a failed or cancelled status and should offer an alternative payment method.

8. Do all banks in Europe support Open Banking payments?

No. While PSD2 requires banks to expose APIs, payment initiation capabilities and reliability vary. Not all banks offer the same level of support, which affects consistency across customers.

9. Is Open Banking suitable for all types of merchant payments?

Open Banking works best for specific scenarios such as account funding, invoices, and cost-sensitive transactions. It is less suitable where consumers expect card protections or where consistent cross-border experience is critical.

10. Should merchants replace cards with Open Banking payments?

In most cases, no. Open Banking works best as a complementary payment method alongside cards and wallets. Using both allows merchants to balance cost, coverage, and customer preference across different markets.

Leave a Reply