Refunds and disputes are where payment methods stop looking similar. At checkout, a card payment and a bank transfer may both feel like simple ways to move money. When something goes wrong, the difference becomes structural.

In the UK, card payments sit inside a long-established dispute framework that assumes disagreement, delay, and reversal as normal possibilities. Bank transfers do not. They are designed around finality, not remediation. That distinction shapes everything that follows from customer expectations to merchant operations and risk exposure.

This blog looks at how refunds and disputes actually work for UK card payments and bank transfers, and why merchants experience them so differently once the transaction has already happened.

Refunds and Disputes for Card Payments in the UK

The scheme-led dispute framework

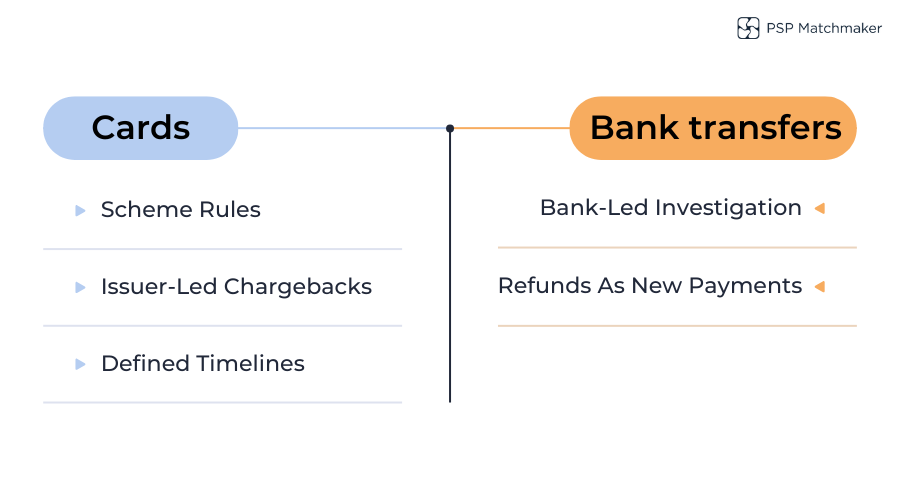

Card payments in the UK sit inside a formal dispute framework defined by card schemes such as Visa and Mastercard. This framework exists because card payments are pull-based and designed to be reversible when disagreements arise.

When a dispute is raised, it follows a recognised path. Reason codes define the nature of the claim, timelines are pre-set, and responsibilities are clearly allocated between issuer, acquirer, and merchant.

Issuer control and merchant response rights

The issuing bank leads the dispute process. A chargeback is initiated, and the transaction amount is often provisionally debited while the case is reviewed. Merchants are not sidelined in this process. They are given the opportunity to respond, submit evidence, and challenge the claim within scheme-defined windows.

Although disputes can be disruptive, the process itself is predictable. Merchants generally know what information will be requested, how long the review may take, and what outcomes are possible. That predictability is a defining feature of card-based dispute handling.

Refunds and Disputes for UK Bank Transfers

Push payments and the absence of a dispute framework

UK bank transfers operate on a push-payment model. The customer instructs their bank to send funds, and once executed, the payment is treated as complete. There is no scheme-level dispute framework comparable to cards.

This means disputes do not trigger automatic reversals. There are no reason codes, no structured timelines, and no central ruleset governing outcomes.

Refunds as new transactions and bank-led reviews

Refunds for bank transfers are processed as new outbound payments initiated by the merchant. They are operational actions, not reversals of the original transaction.

If a customer reports an error or suspected fraud, investigations are led by banks rather than a central scheme. Reviews focus on whether the payment was authorised correctly, misdirected, or influenced by fraud. Recovery is not guaranteed, and outcomes depend heavily on timing, cooperation between banks, and whether funds remain available.

From a merchant perspective, disputes around bank transfers are less visible, less controllable, and far less predictable than card disputes.

Key Structural Differences Between Cards and Bank Transfers

The contrast between cards and bank transfers is not procedural it is architectural. Cards are pull payments. They assume the possibility of reversal. Bank transfers are push payments. They assume finality.

Cards operate within scheme protection. Bank transfers do not. Cards support formal disputes with defined visibility and timelines. Bank transfers rely on ad hoc investigation and cooperation between banks.

As a result:

- Reversal is expected in card payments

- Refunds are discretionary in bank transfers

- Dispute outcomes are more predictable with cards

- Resolution paths for transfers are uncertain by default

These differences shape merchant risk far more than transaction speed or cost ever could.

Operational Impact on Merchants

For merchants, refunds and disputes are not just financial events. They are operational workflows. With cards, customer support teams follow established paths. Evidence requirements are known. Case statuses can be tracked. Accounting systems are built to expect provisional debits and reversals.

With bank transfers, the burden shifts. Merchants must execute refunds manually, reconcile outbound transfers, and manage customer communication without clear timelines. Record-keeping becomes critical, because evidence standards vary by bank and scenario.

Resolution times are uncertain. Some cases close quickly. Others linger without clear updates. This requires different internal processes, different customer messaging, and a higher tolerance for ambiguity.

Risk and Monitoring Considerations

Risk monitoring also diverges sharply between the two methods.

Card payments are monitored using chargeback ratios and dispute thresholds. These metrics directly influence merchant standing with PSPs and acquirers.

Bank transfers do not generate chargebacks, but they are not ignored. Refund behaviour, transaction patterns, and fraud signals are still monitored. PSPs assess whether refund volumes or error rates indicate operational or customer risk.

In both cases, oversight continues beyond individual transactions. The difference lies in how risk is measured and what triggers intervention.

When Each Payment Method Is Typically Used

Cards are typically used where customers expect protection and flexibility. Recurring payments, delayed fulfilment, and consumer-facing services rely on the dispute framework cards provide.

Bank transfers are more common in flows where finality is preferred. Account funding, balance top-ups, and chargeback-averse transactions benefit from explicit customer authorisation and reduced post-payment ambiguity.

These usage patterns are not accidental. They reflect what each payment method is structurally designed to handle when things do not go to plan.

What Merchants Should Understand

Refund and dispute handling is not a policy choice. It is a property of the payment method itself.

Customer expectations differ depending on how they paid. Internal processes must adapt accordingly. Supporting both cards and bank transfers means running parallel workflows, not a single unified one.

Merchants who ignore this distinction often discover it only after the first serious dispute.

Conclusion

Refunds and disputes expose the real differences between card payments and UK bank transfers. Cards are built for disagreement. Bank transfers are built for certainty. Neither approach is inherently better but each carries consequences that surface only after the payment is complete.

For merchants, the risk is not choosing the wrong method, but applying the wrong expectations. Card disputes follow rules. Bank transfer investigations do not. Refunds on cards are procedural. Refunds on transfers are operational decisions.

Understanding these realities allows merchants to design payment flows, customer support processes, and risk controls that align with how each method actually behaves not how similar they appear at checkout.

FAQs

1. Are refunds handled the same way for card payments and bank transfers in the UK?

No, card refunds and disputes follow a scheme-defined process, while bank transfer refunds are handled as new outbound payments initiated by the merchant.

2. Why do card payments support chargebacks but bank transfers do not?

Card payments are pull-based and designed to allow reversals. Bank transfers are push payments, which assume finality once funds are sent.

3. Can a UK bank transfer be reversed if a customer reports a problem?

Not automatically. Banks may investigate errors or fraud, but recovery is not guaranteed and depends on timing and fund availability.

4. Who controls the dispute process for card payments?

The issuing bank leads the dispute process under card scheme rules. Merchants can respond and submit evidence within defined timelines.

5. Do merchants have visibility over bank transfer disputes?

Limited visibility. Unlike card disputes, bank transfer investigations are handled bank-to-bank and often provide fewer status updates to merchants.

6. How do refunds for bank transfers affect merchant operations?

Refunds must be processed manually as new transfers, requiring additional reconciliation, customer communication, and record-keeping.

7. Are bank transfers safer for merchants because there are no chargebacks?

They reduce chargeback exposure, but they introduce other risks, such as limited recovery options and greater responsibility for refund handling.

8. How are disputes monitored for card payments?

Card disputes are tracked using chargeback ratios and thresholds, which directly influence PSP and acquirer oversight.

9. Do PSPs monitor refund behaviour for bank transfers?

Yes. Even without chargebacks, refund volumes and transaction patterns are monitored as indicators of operational or fraud risk.

10. Should merchants use the same support process for both payment methods?

No. Cards and bank transfers require different customer support workflows due to differences in dispute rights, timelines, and outcomes.

Leave a Reply