Card payments in the UK often feel instantaneous. A customer taps or clicks, a confirmation appears, and the transaction seems complete. In reality, that moment is only the beginning of a longer process that unfolds in stages, often out of sight. Authorisation, settlement, and monitoring each serve a different purpose, happen at different times, and involve different decision-makers. Understanding how these stages connect and where they remain deliberately separate helps merchants interpret approvals, delays, and post-payment reviews more realistically.

Key Participants in UK Card Payment Processing

A UK card payment does not move through a single system. It passes between several participants, each responsible for a specific decision or action.

The cardholder and their issuing bank sit on one side of the transaction. The issuer decides whether a payment should be allowed and under what conditions. On the other side, the merchant works with an acquiring bank, often via a PSP, to submit transactions and receive funds.

Between them sit the card schemes, which provide the routing rules and messaging standards that allow issuers and acquirers to communicate. PSPs act as the integration and orchestration layer, shaping how payments are submitted, authenticated, and reported.

No single participant controls the full lifecycle. That fragmentation is intentional and it explains why outcomes sometimes feel inconsistent from a merchant’s perspective.

Card Payment Authorisation in the UK

Authorisation is the first real decision point in a card payment, and it happens quickly. When a transaction is submitted, the issuer evaluates whether to approve or decline it in real time.

At this stage, the issuer checks a combination of basic validity and risk signals. These typically include whether the card is active, whether funds or credit are available, and whether the transaction aligns with expected behaviour. Fraud and risk models run in parallel, often invisibly.

What matters operationally is this: authorisation confirms permission, not completion. An approved transaction means the issuer is willing to honour the payment at that moment. It does not mean funds have moved, nor does it guarantee that nothing will change later.

Factors Influencing Authorisation Outcomes

Authorisation decisions are rarely binary in intent, even though they appear binary in outcome.

Issuers apply their own risk models, thresholds, and controls. The same transaction amount, at the same merchant, can be treated differently depending on issuer policy or customer history. Authentication plays a role too; when additional verification is triggered, successful completion can improve approval odds, while failure leads to decline.

Context matters. Amount, merchant category, customer behaviour, device signals all feed into the decision. This is why merchants often see approval patterns vary by bank or country, even when their own setup remains unchanged.

Settlement of Card Payments in the UK

Settlement happens after authorisation, but it does not happen immediately. Once a transaction is authorised, it enters a clearing and settlement process involving the issuer, the card scheme, and the acquirer. Transaction data is exchanged, obligations are netted, and funds are prepared for transfer between institutions.

Timing varies. Some acquirers settle daily, others on different cycles. PSP arrangements and merchant agreements further influence when settlement completes. Crucially, settlement is a back-office process. It does not involve the customer and is not visible at checkout.

This separation is deliberate. It allows payments to scale, but it also creates a gap between customer approval and merchant fund availability.

Funds Flow to the Merchant

From the merchant’s perspective, the payment lifecycle becomes tangible only when funds are credited.

The gross transaction value is processed first. Fees, charges, and other agreed deductions are then applied before net funds are transferred to the merchant account. The timing of this payout depends on settlement cycles and the payout schedule defined in the merchant agreement.

This is why two merchants processing identical transactions can experience different cashflow timings. The card payment itself may behave the same way, but the commercial and operational layers around it do not.

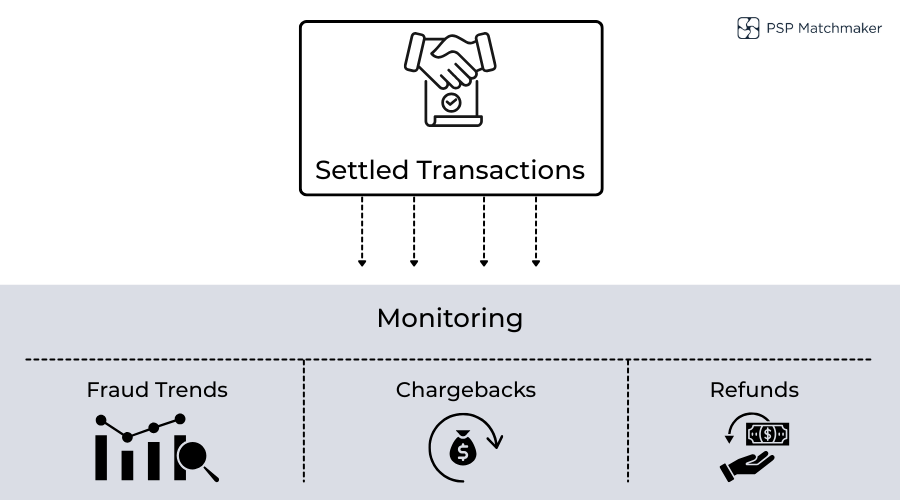

Ongoing Monitoring After Card Payments

Monitoring does not stop once a payment settles. In many ways, it intensifies. PSPs and acquirers are required to monitor transaction patterns across time, not just individual payments. Fraud trends, chargeback ratios, and refund behaviour are reviewed continuously. These signals are assessed in context, not in isolation.

Monitoring obligations apply throughout the merchant relationship. They exist to identify emerging risks, not to judge single transactions. From the merchant’s perspective, this means scrutiny can increase even when day-to-day payments appear to be processing normally.

How Monitoring Can Affect Merchant Operations

When monitoring identifies elevated or changing risk, the impact is operational.

Merchants may see transaction limits adjusted, review frequency increased, or requests for additional information. In some cases, payment acceptance conditions are modified to reduce exposure, such as restricting certain transaction types or geographies.

These changes are often reactive rather than punitive. They reflect how acquirers and PSPs manage ongoing risk under regulatory obligations. However, they can still affect conversion, cashflow, and customer experience if not anticipated.

What Merchants Should Understand About the UK Card Payment Lifecycle

Authorisation, settlement, and monitoring are connected, but they are not the same process. Approval at checkout does not guarantee immediate funds, and successful settlement does not end scrutiny.

Outcomes depend on multiple layers:

Issuer behaviour at authorisation

PSP and acquirer implementation

Merchant activity patterns over time

Merchants who understand these layers are better positioned to interpret declines, delays, and reviews without assuming something has gone “wrong”.

Conclusion

UK card payments are often described as fast and familiar, but their underlying lifecycle is deliberately segmented. Authorisation answers whether a payment can proceed. Settlement determines how and when money moves. Monitoring evaluates what those payments look like over time.

For merchants, problems arise when these stages are treated as a single event. Approval does not mean finality, and settlement does not mean the end of oversight. Each stage serves a different risk and operational purpose, owned by different participants.

Understanding this separation does not remove complexity, but it does remove surprise. Merchants who recognise where decisions are made and when are better equipped to manage cashflow, interpret approval behaviour, and respond calmly when monitoring activity increases.

FAQs

1. Is a card payment complete once it is authorised?

No. Authorisation only confirms that the issuer has approved the transaction at that moment. Settlement and fund movement happen later, through a separate process.

2. Who makes the final decision to approve or decline a card payment?

The issuing bank makes the final authorisation decision. PSPs and acquirers submit the transaction, but issuers control approval logic.

3. Why do some authorised payments settle later than expected?

Settlement timing depends on the acquirer, PSP setup, and the merchant’s agreement. Authorisation and settlement are deliberately separate stages.

4. Can an authorised card payment still be reversed later?

Yes, Even after settlement, transactions can be disputed or charged back if issues arise, which is why monitoring continues beyond payment completion.

5. Why do approval rates differ between issuers for the same transaction?

Issuers apply different risk models, thresholds, and authentication requirements. The same transaction can be treated differently depending on the issuing bank.

6. How long does it usually take for merchants to receive funds?

There is no single timeline. Payout timing depends on settlement cycles and payout schedules agreed with the acquirer or PSP.

7. What does post-payment monitoring actually involve?

Monitoring includes reviewing fraud patterns, chargeback ratios, and refund behaviour across time, not individual transactions in isolation.

8. Can monitoring affect merchants even if payments are processing normally?

Yes, monitoring looks for trends rather than failures. Changes in behaviour can trigger reviews or adjustments without any visible checkout issues.

9. Why are merchants sometimes asked for additional information after onboarding?

Ongoing monitoring obligations require PSPs and acquirers to reassess risk periodically. Requests usually relate to changes in activity rather than past issues.

10. Does settlement mean the end of PSP oversight?

No. Settlement completes the financial leg of a transaction, but monitoring and risk management continue for as long as the merchant relationship exists.

Leave a Reply