Brazil has become one of the most closely watched digital payments markets globally, not because of gradual innovation, but because of how quickly consumer behaviour has shifted. At the centre of that shift is PIX, a real-time payment system operated by the country’s central bank. Since its launch, PIX has moved from a new payment option to an everyday default for millions of Brazilians.

Unlike many instant payment systems that evolved from private-sector initiatives, PIX was designed, launched, and governed centrally, with universal participation built in from the start. That approach has shaped how quickly consumers and merchants adopted it and how broadly it is used today.

This blog explains how PIX works at a system level and explores how consumers and merchants in Brazil are actually using it in practice, across both physical and digital payment scenarios.

What PIX Is and How the System Is Structured

PIX is often described as an instant payment method, but its impact in Brazil comes from how the system itself is designed and governed. Unlike many payment rails that evolved through private-sector collaboration, PIX was built as a national infrastructure with a single set of rules and standards. Understanding its structure helps explain why it scales so effectively across banks, PSPs, merchants, and consumers alike.

Central bank–operated infrastructure

PIX is operated and governed by the Central Bank of Brazil, giving it a unique position in the Brazilian payments ecosystem.

Rather than sitting on top of existing bank transfer rails, PIX functions as a dedicated, real-time payment infrastructure with national scope.

Participation is not limited to banks alone. Payment institutions and PSPs connect directly to the system, allowing broad access while maintaining consistent rules and standards.

Core characteristics of the PIX system

At a structural level, PIX is defined by a small number of design choices that shape how it behaves:

Real-time, account-to-account payments

Continuous availability, including nights and weekends

Direct participation by banks and licensed PSPs

Standardised messaging and settlement rules

Centralised governance and oversight

Because the infrastructure is shared and standardised, PIX does not fragment by provider or region. Every transaction follows the same core rules, regardless of which bank or payment institution the consumer or merchant uses.

How PIX Payments Work in Practice

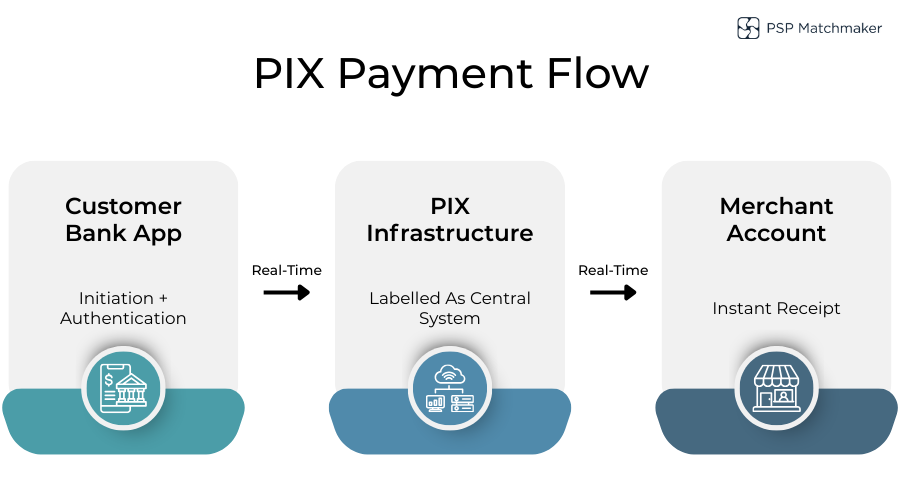

From a user perspective, PIX payments feel simple and immediate. Behind that simplicity sits a clearly defined flow that removes many of the layers typically associated with electronic payments. Looking at how payments are initiated, approved, and completed in practice helps clarify why PIX feels different from cards or traditional bank transfers.

Payment initiation and customer approval

PIX payments are initiated directly by the payer, most commonly through a bank or payment app. Consumers can start a payment by scanning a QR code or by using a PIX key, which acts as a simplified identifier linked to an account.

Authentication happens inside the customer’s own bank environment. The bank confirms identity, validates the payment, and submits it to the PIX system. There is no separate scheme-layer approval or delayed authorisation step.

Confirmation and settlement

Once approved, the payment is processed in real time. Both payer and recipient receive confirmation almost immediately, and funds move directly between accounts.

Settlement is handled within the PIX infrastructure itself, removing the distinction between authorisation and settlement that exists in card payments. From the user’s perspective, confirmation and completion happen as a single event, reinforcing the sense of immediacy and finality.

How Consumers in Brazil Use PIX

PIX adoption among Brazilian consumers did not happen in a single category of payments. Instead, it spread across everyday financial activities where speed, certainty, and ease of use mattered most.

Examining the most common consumer use cases shows how PIX moved beyond novelty to become part of routine payment behaviour.

For Brazilian consumers, PIX has become part of everyday financial behaviour rather than a specialised payment method. Its appeal lies in how quickly it fits into existing habits while removing friction from common transactions.

Consumers most commonly use PIX for:

Peer-to-peer transfers between friends and family

Paying household bills and local services

Making purchases in-store and online

Prioritising speed and simplicity over payment choice

Reducing reliance on cash and, in some cases, cards

Because payments are immediate and bank-authenticated, consumers tend to view PIX as both convenient and trustworthy. Over time, this has normalised its use even for small-value, everyday transactions that previously relied on cash or debit cards.

How Merchants Are Using PIX Today

For merchants, PIX is not just another payment option but a tool that changes how payments are accepted and confirmed. Its real-time nature and push-payment structure influence everything from checkout design to fulfilment timing. Looking at how merchants use PIX across channels reveals why adoption has been so broad.

Everyday acceptance across channels

Merchants in Brazil have adopted PIX across both physical and digital environments. In-store, QR codes allow customers to initiate payments quickly without specialised hardware. Online, PIX is increasingly offered as a checkout option alongside cards.

Merchants use PIX in several practical ways:

- Accepting in-store payments via static or dynamic QR codes

- Supporting account funding and balance top-ups

- Benefiting from instant payment confirmation

- Reducing exposure to card disputes and chargebacks

The immediacy of confirmation allows merchants to release goods or services quickly, particularly in digital contexts. At the same time, the push-payment structure limits post-payment disputes, changing how merchants think about risk and reconciliation.

Why PIX Has Achieved Rapid Adoption in Brazil

PIX’s rapid rise was not accidental, nor was it driven by a single advantage. Its adoption reflects a combination of regulatory design, infrastructure decisions, and user incentives that aligned unusually well.

Breaking down these drivers helps explain why PIX scaled nationally in a matter of years rather than decades.

Mandated participation and national reach

One of the defining factors behind PIX’s rapid adoption is its central bank–led rollout. Major banks were required to participate from the outset, ensuring nationwide availability rather than fragmented coverage.

Cost structure and consumer incentives

PIX transactions are typically free for consumers, removing a key barrier to experimentation and repeat use. With no per-transaction fees visible to the payer, consumers had little reason not to try the system once it became available.

Simplicity and trust

The user experience is intentionally simple. Payments are initiated inside trusted bank apps, with clear confirmation and immediate results. For many users, this feels safer than entering card details or relying on third-party wallets.

Broad merchant acceptance

Adoption accelerated as acceptance spread beyond large retailers to small businesses, service providers, and informal merchants.

PIX works for street vendors and national platforms alike, reinforcing its role as a universal payment method rather than a niche alternative.

Together, these factors created a feedback loop: widespread availability drove usage, growing usage drove acceptance, and acceptance reinforced trust. That cycle explains why PIX moved from launch to ubiquity far faster than most payment innovations.

Conclusion

PIX has become a core payment method in Brazil not because it replaced existing options overnight, but because it aligned closely with how consumers and merchants already wanted payments to work. Its real-time, bank-led design removed friction from everyday transactions while maintaining trust through central oversight.

Today, consumers use PIX for transfers, bills, and purchases with equal confidence. Merchants rely on it for instant confirmation, simplified acceptance, and reduced dispute exposure. The system’s success reflects the impact of combining national infrastructure, universal participation, and a straightforward user experience.

For businesses operating in Brazil, understanding how PIX works and how it is used in practice is no longer optional. It is fundamental to participating effectively in one of the world’s fastest-evolving payments markets.

FAQs

1. Is PIX a private payment system or a government initiative?

PIX is operated and governed by the Central Bank of Brazil, making it a central bank–run payment infrastructure rather than a private scheme. This governance model is a key reason for its rapid nationwide adoption and standardisation.

2. Are PIX payments instant for both consumers and merchants?

Yes, PIX payments are processed in real time, with confirmation delivered almost immediately to both the payer and the recipient. Funds move directly between accounts, removing delays typically associated with settlement cycles.

3. Do consumers pay fees when using PIX?

For consumers, PIX transactions are generally free. This absence of visible transaction costs has played a major role in encouraging everyday usage across different payment scenarios.

4. How do consumers usually initiate a PIX payment?

Most consumers initiate PIX payments through their bank or payment app, either by scanning a QR code or by using a PIX key linked to the recipient’s account. Authentication takes place within the user’s own bank environment.

5. How does PIX differ from card payments for merchants?

Unlike card payments, PIX is a push-based payment method. There are no chargebacks, and payment confirmation is immediate. This changes how merchants think about risk, reconciliation, and fulfilment timing.

6. Is PIX used only for small or informal payments?

No. While PIX is widely used for peer-to-peer and small-value payments, it is also accepted by large retailers, e-commerce platforms, and service providers. Its use spans both informal and commercial transactions.

7. Can PIX be used for online payments as well as in-store?

Yes. PIX is commonly used in physical stores via QR codes and increasingly offered as an option at online checkout, particularly for one-off and account-based payments.

8. Has PIX reduced the use of cash and cards in Brazil?

PIX has significantly reduced reliance on cash and has altered card usage patterns in some contexts. Rather than eliminating other methods, it has become a strong alternative for everyday transactions where speed and certainty matter.

Leave a Reply