Payments in the UK do not operate in a vacuum. Behind every checkout flow, onboarding process, and monitoring requirement sits a regulatory framework that defines how payment services are offered and controlled. At the centre of that framework is the Financial Conduct Authority. While merchants rarely interact with the FCA directly, its oversight has a tangible effect on how PSPs design services, assess risk, and impose operational conditions. This blog explains the FCA’s role in UK payments and how its influence reaches merchants in practice.

The FCA’s Role in the UK Payments Landscape

The FCA’s mandate is not to run payment systems or move money. Its role is to regulate how firms behave when they provide payment services.

Under UK payment legislation, the FCA authorises and supervises payment services firms, including PSPs, e-money issuers, and Open Banking providers. Its focus is on conduct rather than infrastructure.

The FCA does not dictate how fast a payment clears or which rails are used, but it does set expectations around fairness, transparency, and risk management.

Three priorities shape this oversight:

- Consumer protection

- Market integrity

- Financial crime prevention

For merchants, this means that many payment rules they experience are not technical decisions, but conduct-driven ones enforced upstream through regulated providers.

How the FCA Regulates Payment Service Providers

FCA regulation begins long before a PSP offers services to merchants.

Payment firms must be authorised or registered before operating, demonstrating adequate governance, controls, and financial resilience. Approval is not a one-off event. Once authorised, firms are subject to ongoing supervision, periodic reviews, and thematic assessments.

The FCA places particular weight on internal controls:

Senior management accountability

Risk governance structures

Financial crime and AML frameworks

Safeguarding of customer funds

Reporting obligations reinforce this oversight. PSPs must submit regulatory disclosures, incident reports, and compliance updates. When weaknesses are identified, firms are expected to remediate them often by tightening onboarding, monitoring, or transaction controls that merchants later experience as “PSP policy”.

Payment Activities That Fall Under FCA Oversight

The FCA’s remit covers a wide range of payment activities that merchants rely on daily. This includes card payment processing, bank transfer services, and the issuance of electronic money. It also extends to newer services such as payment initiation and account information services under Open Banking.

One area of particular importance is safeguarding. Where PSPs hold or control customer funds, the FCA requires those funds to be protected through segregation or equivalent mechanisms. While merchants may not see safeguarding directly, it influences settlement models, payout timing, and how funds are handled in edge cases.

In short, if a payment activity involves regulated funds or customer access, it likely falls within the FCA’s supervisory scope.

How FCA Regulation Indirectly Affects Merchants

Merchants rarely receive instructions from the FCA. Instead, they experience its influence through the PSPs they work with.

Onboarding standards are a clear example. Documentation requirements, KYB checks, and ownership transparency are shaped by FCA expectations around risk and financial crime. Acceptance decisions are risk-based because PSPs are required to demonstrate that approach to the regulator.

Transaction monitoring follows the same logic. PSPs impose controls, thresholds, and reviews not to inconvenience merchants, but to meet supervisory obligations.

When activity changes, merchants may see limits adjusted, information requests issued, or payment conditions modified.

These controls are not arbitrary. They are the downstream expression of a regulatory framework that holds PSPs accountable for how payment services are delivered and managed.

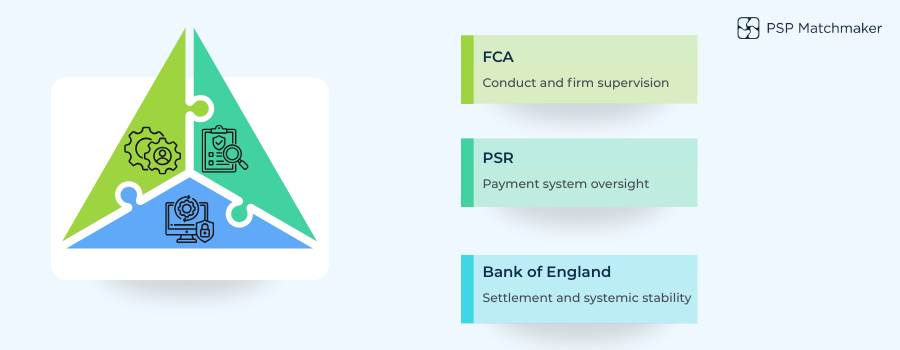

FCA’s Role Compared to Other UK Payment Authorities

The FCA is not the only authority involved in UK payments, and its role is often misunderstood in isolation. The FCA focuses on conduct regulation and firm supervision. It assesses how payment services firms behave, manage risk, and treat customers.

The Payment Systems Regulator looks at payment systems themselves, access, competition, and fairness within schemes and networks.

The Bank of England oversees systemic stability and settlement infrastructure, particularly where financial stability could be affected.

For merchants, these roles intersect, but the FCA’s influence is felt most consistently through PSP behaviour, onboarding standards, and ongoing monitoring expectations.

Conclusion

The FCA plays a defining role in shaping how payment services operate in the UK, even when merchants never deal with it directly. By regulating PSP conduct, governance, and risk management, it sets the conditions under which payments are offered and controlled. Merchants experience this influence indirectly through onboarding, monitoring, and service constraints making an understanding of the FCA’s role essential to navigating the UK payments environment effectively.

FAQs

1. Does the FCA regulate merchants directly?

In most cases, no. The FCA regulates payment service providers, not merchants. Merchants experience FCA influence indirectly through PSP onboarding, monitoring, and operational controls.

2. Why do PSP onboarding requirements feel strict in the UK?

PSPs must meet FCA expectations around financial crime prevention, governance, and risk management. Those obligations flow down into merchant documentation and KYB requirements.

3. Is the FCA responsible for how fast payments are processed?

No. The FCA focuses on conduct and supervision, not payment infrastructure or processing speed. Settlement timing is shaped by systems and commercial arrangements, not FCA rules.

4. Why do PSPs sometimes change limits or payment conditions?

Ongoing FCA supervision requires PSPs to reassess risk continuously. Changes in merchant activity can trigger internal adjustments to remain compliant with regulatory expectations.

5. Does FCA regulation affect all payment methods equally?

Not exactly. While oversight applies broadly, the specific controls differ depending on whether a PSP offers card processing, bank transfers, e-money, or Open Banking services.

6. What is safeguarding, and why does it matter to merchants?

Safeguarding rules require PSPs to protect customer funds. This can influence settlement models, payout timing, and how funds are handled during disputes or operational incidents.

7. How often does the FCA review payment firms?

There is no fixed schedule. Reviews can be ongoing, thematic, or triggered by changes in activity, incidents, or market conditions.

8. Do merchants need to understand FCA rules themselves?

Merchants do not need regulatory expertise, but understanding the FCA’s role helps explain why PSP processes exist and why flexibility is sometimes limited.

9. Is the FCA the same as the Payment Systems Regulator?

No. The FCA supervises firms and conduct. The PSR focuses on payment systems, competition, and access within those systems.

Leave a Reply