The UK is often described as a mature digital payments market, but that maturity does not mean uniformity. UK consumers do not rely on a single payment method. Instead, they move fluidly between cards, bank transfers, and newer Open Banking–enabled options depending on what they are trying to do.

A coffee, a utility bill, a balance top-up, and an online purchase may all be paid for digitally but rarely in the same way. Consumer preference is shaped less by loyalty to a payment method and more by context, familiarity, and perceived protection.

This blog looks at how UK consumers actually use cards, Faster Payments, and Open Banking today. Rather than asking which method is “most popular” in isolation, it explores where each one fits in everyday behaviour and why all three continue to coexist rather than replace one another.

Overview of the UK Consumer Payments Landscape

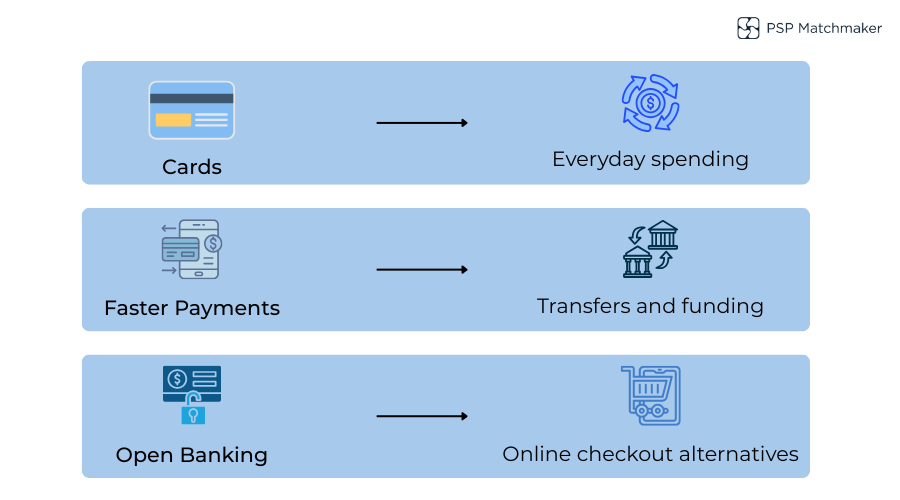

UK consumers sit at the intersection of three strong payment rails. Cards remain deeply embedded in daily life, supported by near-universal acceptance and ingrained habits. At the same time, the UK’s bank transfer infrastructure particularly Faster Payments enables instant account-to-account movement that consumers trust for personal and functional transfers. Alongside these, Open Banking has introduced a newer way to pay directly from a bank account without cards at all.

What’s notable is not competition, but coexistence. There is no single payment method that dominates every use case. Cards excel at everyday spending. Bank transfers dominate peer-to-peer and account movements. Open Banking sits somewhere in between, gaining traction in specific online scenarios.

For consumers, this diversity feels natural. The payment method changes as the situation changes.

Card Payments and Consumer Usage Patterns

Cards remain the most familiar payment tool for UK consumers, particularly debit cards. They are the default choice for everyday spending in-store, online, and increasingly across digital wallets.

Credit cards play a slightly different role. Consumers often reach for them when spending online or making larger purchases, where flexibility and protection matter more than immediacy.

Two expectations underpin card usage:

Familiarity

Cards work almost everywhere, without explanation

Dispute protection

Consumers know there is recourse if something goes wrong

This sense of protection is reinforced by card scheme frameworks from networks such as Visa and Mastercard, even if consumers rarely think about the mechanics.

Cards persist not because they are the newest option, but because they are predictable, widely accepted, and easy to fall back on when uncertainty exists.

Faster Payments and Bank Transfer Usage

Faster Payments underpin a large share of everyday money movement in the UK, even if consumers don’t always label it as such. When people send money to friends, pay bills, or move funds between accounts, they are often using Faster Payments by default.

These are push payments. The customer initiates the transfer from their bank, and funds move in near real time.

Historically, Faster Payments were associated with personal and functional use cases:

Peer-to-peer transfers

For UK consumers, Faster Payments are the default way to send money between individuals. Whether splitting bills, repaying friends, or sending family support, the expectation is immediate movement of funds. The process feels direct and intentional, with little tolerance for delay or uncertainty once the transfer is confirmed.

Regular bill payments

Bank transfers are commonly used for recurring or predictable obligations such as rent, utilities, and council tax. Consumers associate Faster Payments with reliability and control in these contexts, particularly when amounts are known in advance. The absence of card-style dispute protection is accepted as part of that certainty.

Account funding and internal transfers

Consumers frequently use Faster Payments to move money between their own accounts or to fund digital wallets and service balances. Speed is the priority here. The payment is not seen as a purchase, but as repositioning funds, where immediacy matters more than reversibility or consumer protection.

More recently, consumers have become comfortable using bank transfers in merchant contexts, particularly where immediacy matters or where cards feel unnecessary.

What Faster Payments do not offer is dispute comfort. Refunds and reversals are not built into the system, and consumers implicitly understand that once money is sent, it is largely final. That expectation shapes where Faster Payments are and are not used.

Open Banking Payments and Consumer Adoption

Open Banking payments in the UK are most often encountered as Pay by Bank at online checkout, but consumers do not treat them as a general-purpose replacement for cards. Their use is selective and intentional.

What draws consumers in is not novelty, but bank-level authentication. Paying inside a familiar banking app creates a sense of control that feels stronger than entering card details on a third-party site. That reassurance matters most when the merchant is already trusted and the payment is clearly one-off.

Adoption is shaped less by regulation and more by experience. Consumers respond positively when the journey feels contained and predictable, and pull back quickly when it does not.

In practice, uptake tends to be strongest when several conditions align:

Clear positioning at checkout

Familiar bank authentication screens

One-off or time-bound payments

High trust in the merchant

Minimal redirection friction

Open Banking payments remain situational. They are used deliberately, not casually. Compared to cards, consumer reach is narrower. Compared to Faster Payments, the use case is more commerce-driven. Growth is steady, but it follows confidence and experience rather than habit.

How Consumer Preferences Differ by Payment Context

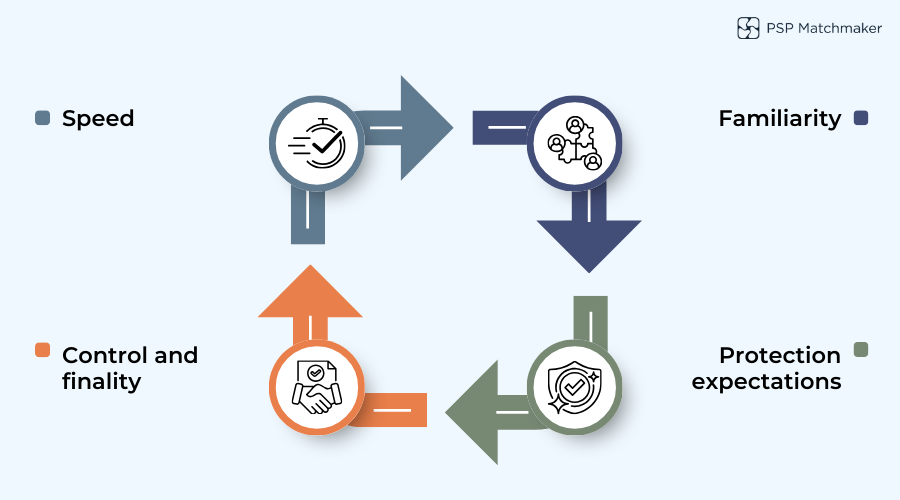

UK consumers rarely think in terms of payment “methods”. They think in terms of outcomes. The choice happens almost subconsciously, shaped by what the payment is meant to achieve.

Everyday spending leans towards cards because they remove friction. Tapping a card or using a stored credential feels effortless, and the presence of consumer protection sits quietly in the background. The method doesn’t demand attention, which is exactly why it works.

When the payment involves moving money rather than buying something, sending funds, paying a bill, topping up an account, Faster Payments take over. These transactions feel purposeful. Consumers expect immediacy and control, and they accept finality as part of that trade-off.

Open Banking tends to appear in more deliberate moments. It is chosen when the payment is intentional, the merchant is trusted, and the customer is comfortable stepping into their bank to approve the transaction.

Consumers switch methods easily because the UK payments ecosystem allows them to. The method follows the moment, not the other way around.

Conclusion

UK consumers do not rely on a single dominant payment method because they do not need to. Cards, Faster Payments, and Open Banking each serve different purposes, and consumers move between them with little friction.

Cards remain central to everyday spending and online commerce, driven by familiarity and protection. Faster Payments underpin real-time account movements where certainty and speed matter more than reversibility. Open Banking is carving out a role in specific online scenarios, offering a direct and bank-authenticated alternative to cards.

Rather than replacing one another, these methods coexist. Their continued use reflects how well the UK payments market supports choice and how consumers intuitively select the right tool for the job. For merchants and payment providers alike, understanding this behavioural reality matters more than identifying a single “most used” method.

FAQs

1. Do UK consumers rely on one dominant payment method?

No. UK consumers regularly switch between cards, Faster Payments, and Open Banking depending on the situation. Usage is context-driven rather than based on loyalty to a single method.

2. Why are cards still so widely used in the UK?

Cards remain familiar, widely accepted, and easy to use for everyday spending. Consumers also value the dispute and refund protections that come with card payments.

3. When do consumers prefer Faster Payments over cards?

Faster Payments are commonly used for peer-to-peer transfers, bill payments, and moving money between accounts. These are situations where speed and control matter more than reversibility.

4. Are UK consumers comfortable using bank transfers with merchants?

Increasingly, yes particularly for account funding and known merchant relationships. However, expectations around refunds and disputes are different from card payments.

5. What drives adoption of Open Banking payments among consumers?

Trust and experience. Consumers are more likely to use Open Banking when checkout messaging is clear, the bank authentication flow feels familiar, and the payment is one-off or intentional.

6. Is Open Banking replacing cards in the UK?

No. Open Banking is being adopted selectively as an alternative at checkout, not as a universal replacement for cards.

7. How important is payment speed to UK consumers?

Speed matters, but only in certain contexts. For transfers and account funding, immediacy is expected. For purchases, familiarity and protection often outweigh raw speed.

8. Do consumers understand the differences between payment methods?

Not always explicitly, but behaviour reflects understanding. Consumers adjust their choices based on expectations around control, protection, and finality.

9. Why do consumers accept fewer protections with bank transfers?

Because bank transfers are typically used in situations where certainty and intent are prioritised. Consumers implicitly accept finality in exchange for speed and control.

10. What should merchants learn from UK consumer payment behaviour?

That no single payment method fits every use case. Supporting multiple options allows consumers to choose what feels right for the moment.

Leave a Reply