Latin America is often discussed as a single payments region, but in practice it operates as a collection of distinct national markets. There is no unified payment infrastructure, no shared clearing system, and no common regulatory framework spanning the region. Each country has built its payment ecosystem around local banking structures, regulations, and consumer behaviour.

As a result, payment integrations that work in one market rarely translate directly to another. This blog explains why payment integrations differ so widely across Latin America and highlights the structural factors that make regional standardisation difficult.

Fragmented Payment Infrastructure Across Latin America

Payment infrastructure across Latin America has developed independently within national borders rather than through regional coordination. Each country has built its own systems to serve domestic priorities, resulting in structural differences that persist today. Looking at how infrastructure is owned, connected, and settled at a country level helps explain why payment integrations cannot be standardised across the region.

Nationally designed payment systems

Latin America does not have a regional payment rail equivalent to SEPA or Faster Payments. Instead, payment infrastructure has been designed and implemented at a national level, with each country prioritising domestic requirements over regional interoperability.

Banking connectivity and settlement models

Countries operate their own clearing and settlement systems, often owned or overseen by central banks or domestic banking consortia. Connectivity models vary, with some markets supporting direct bank integrations while others rely on intermediaries.

Infrastructure shaped by local priorities

Because infrastructure decisions were made independently, differences emerged in operating hours, settlement cycles, message formats, and technical standards. These systems work effectively within national borders but do not align easily across countries, creating inherent integration differences for merchants operating regionally.

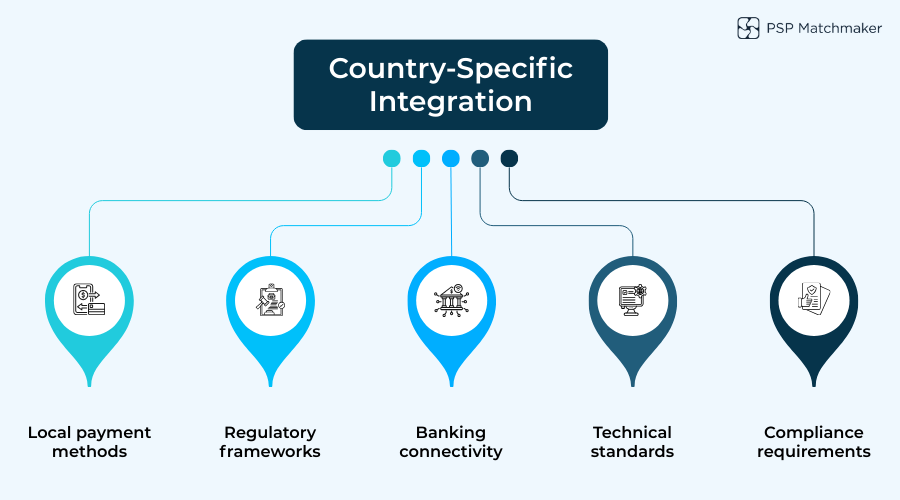

Local Payment Methods Drive Integration Differences

Local payment methods are one of the most visible reasons integrations differ across Latin America, but the complexity goes deeper than surface-level variation. Each market has developed its own mix of instant payments, bank transfers, wallets, and card behaviours, all supported by unique technical standards. Breaking these down shows why integrations must be tailored country by country.

Instant payments and bank transfers

Many countries have introduced instant payment systems, but each operates independently with unique rules and technical requirements. Bank transfer formats, identifiers, and confirmation mechanisms differ by market, preventing reuse of a single integration.

Wallet and card localisation

Wallet ecosystems are highly market-specific, shaped by local providers, funding models, and consumer trust. Card schemes, while global, are also localised through domestic routing, instalment features, and regulatory requirements.

These differences surface in several ways:

Country-specific instant payment systems

Local bank transfer formats and identifiers

Distinct wallet ecosystems by market

Card scheme localisation and domestic routing

Unique technical standards and message structures

As a result, merchants must integrate not just different methods, but different interpretations of what a “payment” looks like in each country.

Regulatory and Compliance Variations by Country

Regulation plays a decisive role in shaping how payments are integrated and operated in Latin America. Rather than a shared framework, each country applies its own licensing, compliance, and data requirements. Understanding how regulatory authority is structured and how it differs by market clarifies why integrations must adapt beyond technical considerations alone.

National regulators and licensing frameworks

Payment regulation in Latin America is set at the country level. Central banks and financial regulators define who can offer payment services, under what licence, and with which operational constraints.

Local compliance requirements

KYC and AML obligations vary significantly across markets. Documentation standards, verification thresholds, and ongoing monitoring requirements are shaped by local risk assessments rather than regional alignment.

Data, limits, and controls

Some countries impose data localisation rules, affecting where transaction data can be stored or processed. Transaction limits, reporting obligations, and consumer protection rules also differ, influencing how payment flows must be designed.

These regulatory differences directly affect integration scope, data handling, and operational workflows. Even when payment methods appear similar on the surface, compliance requirements often force divergent technical implementations.

Banking Access and Technical Readiness

Beyond regulation, differences in banking technology play a major role in shaping integrations.

Banks across Latin America vary widely in technical maturity. Some markets support modern APIs and real-time connectivity, while others rely on legacy systems with limited automation and restricted operating hours.

Key factors influencing integration readiness include:

Varying bank API maturity

Legacy versus modern core banking systems

Differences in uptime and reliability

PSP dependence on local bank partners

Extended integration testing cycles

These disparities mean that integrations must often be adapted to the least flexible participant in the chain, increasing development effort and reducing standardisation.

How These Differences Affect Merchant Payment Setup

The combined effect of infrastructure, payment methods, regulation, and banking readiness ultimately surfaces at the merchant level. What may appear as integration “complexity” is often the direct result of adapting to multiple local realities. Examining how these differences affect merchant payment setup helps explain why regional expansion is rarely straightforward.

Integration and provider complexity

For merchants, structural differences translate into practical challenges. Rather than building one regional integration, businesses often need separate setups for each country, sometimes supported by different PSPs or banking partners.

Slower regional scaling

Expanding into a new Latin American country frequently requires new technical work, regulatory assessment, and operational preparation. This slows regional rollout and increases dependency on local expertise.

These effects are not the result of merchant choices, but of the underlying payment landscape each market operates within.

Conclusion

Payment integrations differ across Latin America because the region was never designed to function as a single payments market. Infrastructure, regulation, banking connectivity, and payment methods have all evolved independently at the country level, creating structural differences that merchants must accommodate.

These differences are not driven by merchant requirements or PSP preferences, but by national priorities and local market realities. Even where payment methods appear similar, underlying rules and technical standards often diverge.

For businesses expanding across Latin America, recognising this fragmentation is essential. Successful payment strategies are built around local integration realities rather than assumptions of regional uniformity. By planning for country-specific requirements from the outset, merchants can reduce friction, manage complexity, and scale more effectively across one of the world’s most diverse payment landscapes.

FAQs

1. Why can’t merchants use a single payment integration across Latin America?

Because Latin America does not have a unified payment infrastructure. Each country operates its own payment rails, banking connectivity models, and regulatory frameworks, which makes a single, reusable integration impractical.

2. Are payment integration differences mainly technical or regulatory?

They are both. Technical differences arise from local payment systems and bank readiness, while regulatory differences stem from country-specific licensing, compliance, and data requirements. In most cases, the two are tightly linked.

3. Do instant payment systems reduce integration complexity in LATAM?

Instant payment systems can simplify domestic payments, but they are country-specific and not interoperable across borders. As a result, they often increase regional integration complexity rather than reduce it.

4. Why do local payment methods affect integration so heavily?

Local payment methods define identifiers, message formats, confirmation behaviour, and settlement logic. Even when two methods serve a similar purpose, their technical and operational requirements are rarely aligned across countries.

5. How do banking systems influence payment integrations?

Banks across Latin America vary in technical maturity. Some support modern APIs and real-time connectivity, while others rely on legacy systems. Integrations must often be adapted to the least flexible participant in the chain.

6. Does regulation directly change how payments are integrated?

Yes. Licensing requirements, KYC and AML rules, transaction limits, and data localisation laws all influence how payment flows must be designed and implemented at a technical level.

7. Why do merchants often need multiple PSPs in Latin America?

No single PSP typically offers full coverage across all LATAM markets with consistent capabilities. Merchants often rely on multiple providers to achieve acceptable reach, performance, and compliance.

8. Is integration complexity a sign of an immature payments market?

Not necessarily. Much of the complexity reflects deliberate national design choices rather than lack of sophistication. Each market optimised its systems for domestic needs rather than regional uniformity.

Leave a Reply